From Unsecured to Influential: Homebuyers Gain Ground Under IBC Reforms

- Homebuyers gain stronger representation in insolvency proceedings, with improved participation in the Committee of Creditors (CoC).

- Possession rights protected – Completed flats can be handed over during insolvency, and occupied units are safeguarded from liquidation.

- CIIRP introduced under the Insolvency and Bankruptcy Code, enabling faster, largely out-of-court resolution with a debtor-in-possession model.

- Project-specific insolvency allowed, ensuring stalled real estate projects can be resolved independently without affecting viable developments.

- Greater regulatory oversight via Real Estate (Regulation and Development) Act (RERA) participation and mandatory transparency from Resolution Professionals.

- Overall shift in policy approach – Homebuyers are no longer passive unsecured creditors but recognized as key stakeholders in stressed real estate resolutions.

The Insolvency and Bankruptcy Code (IBC) stands as the central pillar of the Indian corporate insolvency system since its introduction. The Code has continuously been reshaped to the needs of practical challenges, for effective and timely corporate resolution, through legislative amendments, judicial interpretations, and regulatory refinements.

Among the different corporate insolvency stakeholders, the homebuyers have been the most susceptible to the impact of such insolvency processes. Generally, they have been the minority or unsecured creditors with hardly any voting power in the decision, making under the insolvency proceedings in the favor of the financial institutions that only looked at their own recovery and left the completion of the project to be the problem of homebuyers).

The latest amendments in the IBC especially those made during 2024- 25 have brought radical changes to the situation of homebuyers. The reforms offering increased rights to homebuyers, quickening the resolution pace, and giving room for project, specific recovery methods of stressed real estate projects, thus, represent a major real estate sector shift in the interaction with the insolvency framework.

Background: Challenges in Real Estate Insolvencies

Real estate is a sector that stands out uniquely in the broader insolvency world. Normally, when a company in the corporate world faces the need for a restructuring, merger or liquidation, these actions do not result in any direct negative consequences for customers. However, real estate projects differ in that they are a kind of tangible asset that is closely connected to people's homes and the huge financial commitments involved in them. In case of a developer's failure, the first group of affected people are the homebuyers who have their life savings and future plans tied up in the unfinished property.

For a long time, the IBC system gave the highest priority to financial creditors holding security such as banks and non-bank financial institutions. Homebuyers were categorized as unsecured creditors and were usually found at the bottom of the creditor hierarchy. The Supreme Court as well as different regulatory interventions have been very empathetic towards their situation but, nevertheless, formal insolvency procedures did not give them real power or a role in the decision, making process. Thus, a large number of homebuyers have faced long delays, construction stoppages, and uncertainty as to whether they will finally get possession of their homes.

The changes in 2024-25 reflect the realization that homebuyers are a different kind of stakeholders whose interests are not adequately safeguarded when they are just treated as unsecured creditors. The intended outcomes of the reforms are to set up a system whereby homebuyers will be able to have a say, impact the determination of projects, and get possession without unnecessary delay.

The Insolvency and Bankruptcy Code (Amendment) Bill: Key Features

The IBC amendments brought about a number of structural and procedural changes that would help increase efficiency and participation. The most radical changes are:

- Creditor-Initiated Insolvency Resolution Process (CIIRP): This process enables creditors, especially organized financial creditors, to take the lead in the resolution process, and the courts are less involved in the initial stages of the process. The CIIRP is a largely out-of-court process with judicial intervention at critical points.

- Improved Withdrawal Restrictions: Earlier, the withdrawal of an insolvency application was possible with very limited approvals, which was prone to abuse. The new rules make withdrawals possible only with a strong consensus of creditors, ensuring that only genuine cases are allowed to proceed or are closed.

- Moratorium During Liquidation: The new rules make it clear that once a liquidation process is initiated, the legal proceedings and enforcement of claims are stayed temporarily, safeguarding the interests of all concerned, including homebuyers.

- Faster Timelines and Greater Transparency: The proposed changes seek to minimize the delays that are characteristic of conventional insolvency cases, with a focus on faster timelines, transparency, and accountability.

- Cross-Border and Group Insolvency Provisions: In recognition of the fact that corporate structures can be complex, with global assets, the Code introduces a framework for dealing with cross-border insolvency cases.

- Out-of-Court Resolution Provisions: The proposed changes seek to promote out-of-court resolutions for genuine cases of business failure, relieving the courts of the burden of dealing with such cases while still maintaining statutory protections for creditors and other parties.

- Notwithstanding the general applicability of the proposed changes, they are especially important in the context of distressed real estate projects and homebuyers seeking possession of completed properties.

The Creditor- Initiated Insolvency Resolution Process (CIIRP)

The CIIRP represents a significant change in the insolvency framework, aiming to merge the quickness and agility of out-of- court settlements with the legal authority of court sanctioned procedures. The process emphasis is on efficiency and the cooperation of stakeholders, alongside safeguarding the interests of creditors.

Initiation and Eligibility

The CIIRP has been designed with certain corporate entities in mind, those that satisfy particular regulatory benchmarks, generally the ones that have a large financial exposure and complex operations. Besides, the mechanism shouldn't be initiated if the company is in the middle of other insolvency proceedings or if it has recently been resolved through insolvency resolutions, thus, avoiding procedural overlaps and misuse of the mechanism.

Eligible financial creditors, which are usually well organized institutions having the experience in resolving stressed assets, are entrusted with the responsibility of initiating the process. Before appointing a resolution professional, these creditors must obtain the consent of the majority of the financial creditors in terms of debt value and also notify the debtor, thus giving him/her an opportunity to make his/her representation.

The initiation phase is intentionally structured to reduce court intervention. Even though the National Company Law Tribunal (NCLT) is informed of the matter, it will only get involved if disputes arise or for the final approval of a resolution plan. Such out of court initiation is in line with international best practices and it lessens the wait time that is a frequent feature of court driven processes.

Debtor- in Possession Model

One of the unique aspects of CIIRP is the debtor, in, possession method. The idea behind it is that unlike in a typical CIRP during which control of the corporate debtor is passed to the resolution professional, the incumbent management is allowed to continue running the business under supervision. This model:

Supports the business running without interruptions and especially in the case of construction and project delivery, it is very important.Minimizes the risk of value erosion or cash flow disruptions.Enables the resolution professional to concentrate on checking and helping the resolution rather than taking care of the daily operations.The debtors management is the one responsible for providing the truthful information only and if they knowingly issue false disclosures, they may incur personal liability. The resolution professional also has the power to disapprove of any decisions or resolutions which could be detrimental to the resolution process.

Moratorium and Legal Protection

CIIRP moratoriums are not automatic; they need the consent of creditors or a majority of the financial institutions before they can be put in place. This legality is a loophole that keeps all parties, the homebuyers among them, safe from the filing of new lawsuits and the execution of old ones, thus maintaining a balance between the homebuyers and creditor oversight. Significantly, the moratorium takes effect from the very date of application, thereby providing a remedy that is swift and does not require court approval.

Resolution Timelines and Plan Approval

CIIRP is all about the timely resolution of the matter. Plans that are geared towards a solution must go through the statutory and creditor approval processes, regulatory compliance, and other necessary requirements, even though the process is fast tracked. The failure of the resolution plan to bring about a successful outcome will see the CIIRP being automatically changed into a typical CIRP, thus making sure that the resolution does not come to a halt because of the delay.

Enhancing Homebuyer Rights in Real Estate Insolvencies

The amendments for the years 2024, 2025 are targeted at a more effective participation and protection of homebuyers. Major changes include:

- Possession During Resolution: Homebuyers are allowed to occupy the flats that have been finished during the insolvency process on condition that the creditors' majority agrees. This measure prevents possession delays and, at the same time, ensures that homebuyers get their properties even if the corporate restructuring goes on.

- Project- Focused Insolvency: Insolvency proceedings can be restricted to specific stalled projects instead of the entire corporate entity. This way, the projects which have been completed or are at an advanced stage, will be given priority to be delivered to homebuyers.

- Representation Mechanisms: In large developments with multiple homebuyers, facilitators can be appointed to represent the homebuyers' interests in the CoC. This promotes transparency and ensures that the homebuyers' voices are heard in decisions that impact the completion of the project.

- Resolution Professional Accountability: RPs must provide progress reports and updates to stakeholders on a regular basis, thus fostering accountability and minimizing delays.

- Regulatory Oversight: Officials of RERA will be able to attend the meetings of the CoC, thereby ensuring that the real estate norms and the consumer protection regulations are observed even as the insolvency proceedings are underway.

- Protection from Liquidation: Properties where the possession has been granted but the deeds have not been registered are not part of the liquidation estate. This way, homebuyers will be safeguarded from the scenario of their homes being sold to settle corporate debts.

Creditor-Initiated Insolvency Resolution Process (CIIRP) Impact on Homerbuyer

One of the most revolutionary changes brought about by the 2025 amendments is the Creditor-Initiated Insolvency Resolution Process (CIIRP). CIIRP enables financial creditors to take the lead in the resolution process in a manner that is largely out-of-court, while still maintaining statutory oversight at critical points. In the case of real estate projects, CIIRP brings about the following benefits:

- Debtor-in-Possession Model: In contrast to CIRP, the management structure of the developer remains in place to manage the project, ensuring that construction and project implementation continue uninterrupted.

- Faster Resolutions: Early creditor engagement and less court intervention at the outset result in faster resolution.

- Conversion to CIRP if Required: In the event that the resolution under CIIRP does not succeed, the process smoothly transitions into CIRP, ensuring that statutory safeguards and continuity are maintained.

- Moratorium Flexibility: Statutory safeguards can be invoked immediately upon creditor approval, protecting projects from lawsuits and enforcement actions while the resolution process is underway.

In the case of homebuyers, CIIRP could bring about faster completion of projects, better oversight, and less disruption, assuming that there is creditor and developer cooperation.

Implications for Homebuyers

The net result of these amendments is that homebuyers are no longer mere passive stakeholders. They now have:

- Access to possession in cases of insolvency.

- Representation in CoC meetings through facilitators.

- Protection against the liquidation of occupied apartments.

- Regulatory protection through participation in RERA.

These changes indicate that homebuyers are no longer relegated to the background, as was the case in the past, but are now recognized for their importance as stakeholders in a distressed real estate venture.

Ongoing Challenges and Issues

Despite these progressive changes, home buyers are still faced with the following challenges:

- Creditor Approval Thresholds: Resolutions such as the granting of possession are still subject to the approval of the majority of the creditors. Disputes may arise if financial institutions are more concerned with recovering their debts than with the delivery of homes.

- Unsecured Status in Liquidation: In the strict order of priority, home buyers are still lower than secured creditors and employees in the event of a liquidation.

- Practical Delays: Although there are statutory time limits, practical and administrative issues may cause delays in resolutions.

- Thresholds for Initiating Insolvency: The minimum participation thresholds for home buyers to initiate project-level insolvency may still cause difficulties for smaller projects.

Proposed IBC Amendments Positive but Recovery Rates and Timelines Remain a Concern: As per ICRA

ICRA cautioned that the current set of proposals does not adequately address the real estate and construction sector, which continues to face unique structural challenges under the insolvency framework. The real estate sector has the second-highest share of cases undergoing the corporate insolvency resolution process (CIRP) as of September 30, 2025. Given the government’s sustained focus on protecting homebuyers and resolving stalled housing projects, ICRA believes that targeted and sector-specific reforms will be necessary to meaningfully address insolvency issues in this segment.

IBC Performance After Nine Years

Since its implementation in 2016, the IBC has emerged as India’s most effective institutional mechanism for corporate debt resolution, delivering better realisations for creditors compared to earlier recovery modes. Despite its shortcomings, the framework has enabled cumulative recoveries of approximately ₹4 lakh crore.

The Corporate Insolvency Resolution Process was started for a total of 8,658 corporate borrowers, who entered the Corporate Insolvency Resolution Process (CIRP) as of September 2025. Of these cases, approximately 63% have been closed via a successful resolution plan, withdrawn or withdrawn from the CIRP process, or liquidated. Although the rate at which the cases have been closed has been consistent and positive, recovery from the corporate borrowers has remained low. The average recovery for successful resolution plans is approximately 32% of the value of the creditors' claims.

ICRA noted that prolonged resolution timelines have been a key factor contributing to value erosion. Data indicates that nearly three-fourths of ongoing CIRP cases had exceeded 270 days from the date of admission by the National Company Law Tribunal (NCLT) as of September 30, 2025, despite the mandated outer limit of 330 days, including litigation.

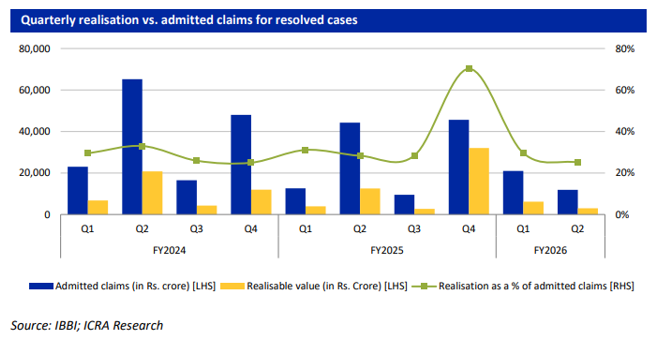

Recovery Rates Weaken in H1 FY2026

After displaying gradual improvement until the fourth quarter of fiscal year 2025, the recovery trends reversed in the first half of fiscal year 2026. The ICRA has observed decreases in the entire volume of recoveries, as well as in recovery as a proportion of the volume of admitted claims. This was observed for all sizes of insolvencies, including the large insolvencies which involved claim amounts greater than ₹1,000 crore.

Claims volume admitted continues to be at a high level, however, the amount expected to be recovered from the volume of admitted claims is not keeping up with new claims, resulting in lower recovery ratios. The slowdown in recoveries has been attributed to a number of issues still being faced by the industry, including delays due to litigation, a limited number of participants bidding for assets within certain cases and/or challenges associated with determining the value of an asset.

Also, the number of approved resolution plans has declined. Presently, only 105 resolution plans have been approved during the first half of fiscal year 2026, as compared to 124 approvals within the same period of time during the first half of fiscal year 2025. Although the number of new insolvencies being admitted has decreased, the lower percentage of resolution approvals indicates that the bottlenecks within the overall IBC system are still occurring.

Homebuyers' Changing Role

The introduction of the IBC clauses and the CIIRP mechanism have opened up the doors for homebuyers to move from the margin to the main stage of real estate project insolvency. Their voice has been amplified by their representation in the CoC. Homebuyers' rights have been acknowledged and they are no longer seen simply as unsecured creditors who are last in the line of priority. Besides, they have also got avenues to own the property even when there are insolvency proceedings.

Homebuyers are not only being provided with project, specific resolution options, but these options have also helped projects to be delivered better. Through the involvement of RERA, homebuyers have been kept under the watch of a regulator. The success of these initiatives is primarily influenced by the willingness and harmony of the stakeholders involved. Homebuyers should lead the way, financial institutions should be inclined towards the fair outcome, and RPs should be transparent and responsible.

At the core, homebuyers are less and less observers and more and more important contributors to corporate insolvency resolutions. If one looks at the scenario as a whole, it is a turning point in real estate insolvency in India as the legal and regulatory framework has provided them with the tools necessary to safeguard their interests, although challenges still remain.

.png)