India's real estate sector witnessed a slowdown in private equity (PE) investments during the first half of 2026, with total inflows declining 23% year-on-year to $1.13 billion, as elevated global interest rates and tighter financial conditions prompted institutional investors to adopt a more selective investment strategy. However, the decline reflected a shift in global capital allocation rather than weakening confidence in India's long-term real estate fundamentals, according to Knight Frank India's latest capital markets report.

The report shows that PE investments fell from $1.47 billion in H1 2025 to $1.13 billion in H1 2026, with capital increasingly flowing towards income-generating commercial assets while residential investments witnessed a sharp contraction.

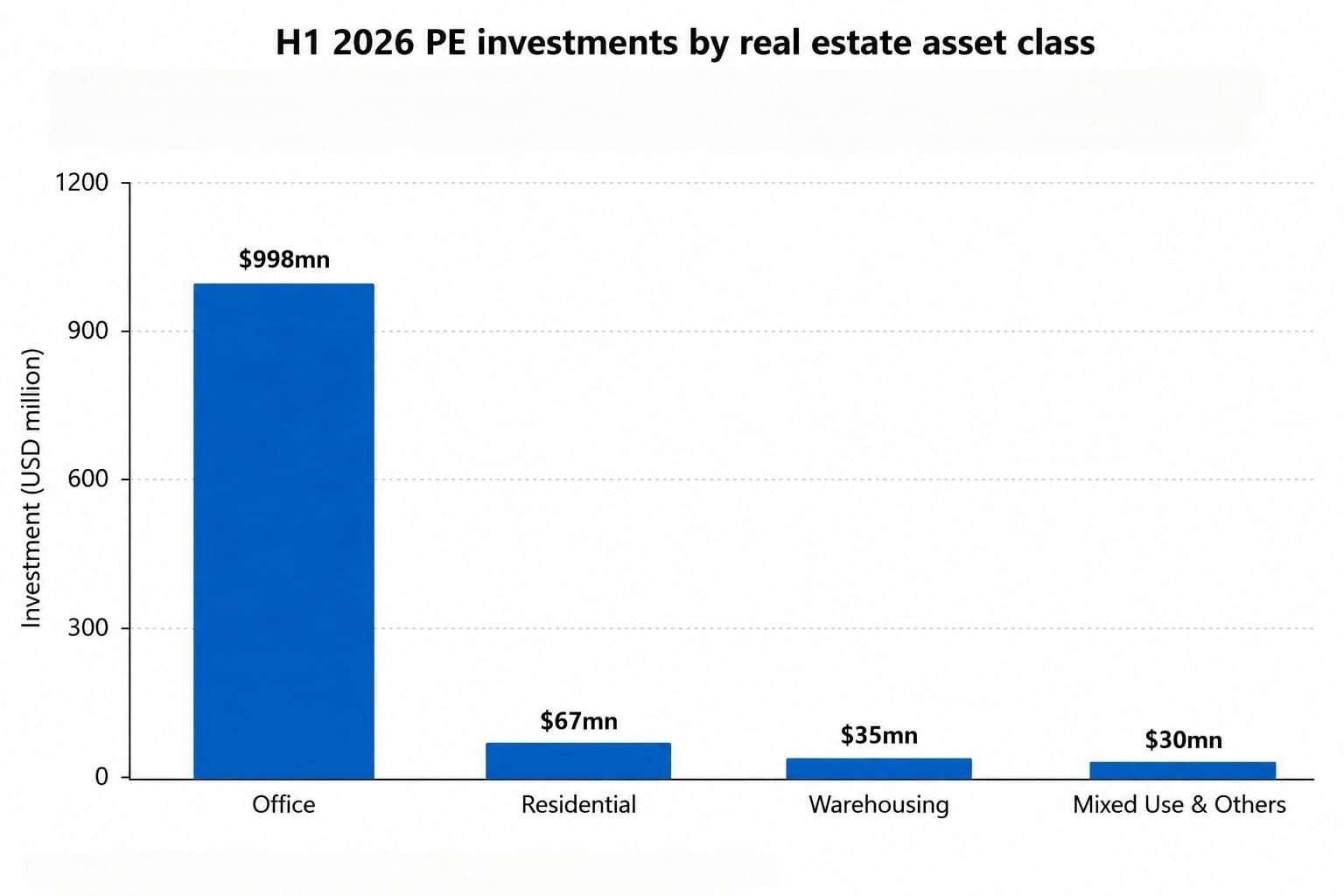

Office Real Estate Attracts Nearly 90% of PE Investments

Despite the overall moderation in investment activity, office real estate remained the clear favourite among institutional investors.

Source: Knight Frank India

The office segment attracted $998 million during the January-June 2026 period, registering a 33% year-on-year increase and accounting for 89% of all PE investments in Indian real estate. The surge was driven by continued expansion of Global Capability Centres (GCCs), strong leasing demand from multinational corporations and domestic occupiers, and growing investor preference for stable rental income.

Investor preferences also shifted towards lower-risk assets. Around 75% of office investments were directed towards completed properties, compared with 53% during the same period last year, highlighting growing demand for operational, income-producing commercial assets amid elevated financing costs and tighter return expectations.

Residential Investments See Sharp Decline

The residential segment experienced one of the steepest corrections during the period.

Private equity investments in housing fell by nearly 50% year-on-year, reflecting investors' cautious stance towards development-led projects that typically involve longer execution timelines and higher construction risk.

While India's housing market continues to benefit from sustained end-user demand, stronger balance sheets among organised developers and increasing market formalisation, global investors have increasingly prioritised assets offering immediate cash flows over under-construction residential developments.

Industry experts believe the moderation in residential PE inflows does not necessarily indicate weakening housing demand but rather reflects changing global investment preferences amid higher borrowing costs.

NCR Emerges as Top Investment Destination

Among India's major property markets, the National Capital Region (NCR) attracted the highest share of PE investments during H1 2026.

The region received approximately $411.1 million, recording an impressive 522% year-on-year increase, accounting for more than one-third of all private equity investments in Indian real estate during the six-month period.

Pune followed with $355.9 million, supported by continued commercial development and industrial expansion. Other major destinations included:

| City | PE Investment (H1 2026) |

| NCR | $411.1 million |

| Pune | $355.9 million |

| Chennai | $154.7 million |

| Bengaluru | $115.9 million |

| Mumbai | $84.3 million |

Global Capital Becoming More Selective

According to Knight Frank India, the moderation in investment volumes reflects changing global financial conditions rather than any deterioration in India's real estate market.

Higher global borrowing costs have narrowed the yield advantage traditionally enjoyed by emerging markets, leading investors to place greater emphasis on risk-adjusted returns, execution certainty and liquidity before deploying capital.

As a result, institutional investors have increasingly shifted their focus towards operational office assets capable of generating stable rental income instead of funding development-stage residential projects.

Industry Sees Strong Long-Term Fundamentals

Commenting on the investment trends, Shishir Baijal, Chairman and Managing Director, Knight Frank India, said,

The decline in PE inflows should not be interpreted as weakening fundamentals of India's real estate sector.

He noted that while higher global interest rates have affected cross-border capital flows, India's office market continues to demonstrate resilience, supported by sustained GCC expansion, robust occupier demand and an expanding pipeline of institutional-grade commercial assets. He added that attracting larger pools of global capital in the coming years would depend not only on strong market fundamentals but also on building a more competitive investment ecosystem.

Outlook

Although overall private equity investments moderated during the first half of 2026, the data suggests that institutional investors remain committed to India's commercial real estate story, particularly office assets offering stable and predictable income streams.

The sharp decline in residential funding highlights growing investor preference for lower-risk, income-generating properties amid an uncertain global interest rate environment. However, analysts expect residential investments to regain momentum once financing conditions improve and global capital markets stabilise.

With India's office leasing market continuing to post healthy demand, supported by multinational corporations and Global Capability Centres, commercial real estate is expected to remain the primary destination for institutional capital in the near term, even as investors closely monitor macroeconomic conditions and interest rate movements.