India's national flex workspace brands continued to maintain a price premium of over 19% of 2021 to 2026. The Report captured India's flex workspace market price trends through five years of transaction data on brands, scale, commitment, and growth of operations of Indian companies. The myHQ Report 2026 covered 1,384 unique centres across 30 cities and tracked booking behaviour of over 10,000 companies.

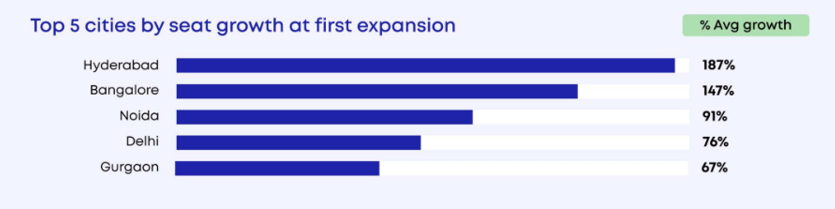

The Pricing Report revealed Hyderabad led the seat growth expansion with 187% average seat growth at first expansion, Bangalore at 147%, Noida at 91%, Delhi at 76% and Gurgaon at 67% growth in seats. The report identified Hyderabad’s growth as an important indicator of how fast enterprise and growth-stage demand is deepening in Indian office markets.

The Report’s data showed that national flex brands WeWork, Awfis, Smartworks, 91Springboard, and Innov8 consistently commanded a significant price premium over independent operators. From 2021 to 2026, national brands charged a median of ₹8,600 per seat per month, compared to ₹7,200 for independents operating in the same locality and quality tier – a difference of ₹1,400 per seat, or a 19% brand premium.

Utkarsh Kawatra, Co-Founder and CEO, myHQ, said, “The 17-20% steady premium range reflects the value enterprises place on predictability and standardized service, much like travelers opting for Marriott or Taj over standalone hotels. is expected to widen further, with the brand premium projected to reach 25% by FY28 as enterprises increasingly consolidate their workspace needs with trusted, multi-city operators. For example, a company choosing WeWork in Bangalore's central business district would pay nearly one-fifth more per seat than at a comparable independent co-working space, purely for the assurance of brand reliability and consistent experience.”

The report also reveals distinct expansion behaviour across different categories of clients. Startups with 1–15 seats showed the steepest growth after their first booking, expanding their seat footprint by an average of 128% within three months. According to the report, this is largely hiring-led growth, where teams outgrow their first office quickly and need additional capacity almost immediately.

MSMEs, defined in the report as companies booking 16–50 seats, expanded more gradually, recording 60% average seat growth over 3.8 months. The report describes this as the most measured expansion pattern, driven less by urgency and more by planned business growth. Larger enterprises, with 51+ seats, expanded by 59% on average and did so the fastest, at 2.7 months, reflecting the growing use of flex as a core workspace strategy rather than a temporary solution.

Another key finding is the direct relationship between lock-in period and pricing. Shorter lock-ins cost companies more, while longer commitments create measurable savings. A 24-month lock-in was found to save companies ₹9,600 per seat annually compared to a six-month lock-in. The median premium for a six-month lock-in under a 24-month commitment was 8.2%.

Scale is another major pricing driver. The report finds that volume discounts in flex workspaces typically do not unlock at small or mid-sized team levels. Instead, they begin to appear when a booking crosses a meaningful scale, especially above the 50-seat mark. At that point, clients can unlock savings of around ₹1,000 per seat per month, translating into a median volume discount of around 12%. For a 60-seat team, this can translate into annual savings of about ₹7.2 lakh. For a 100-seat enterprise booking, to ₹12 lakh, and over a 24-month lock-in, ₹24 lakh.

The report concludes that the next phase of India’s flex workspace market will be shaped by sharper segmentation and more transparent pricing logic. the brand premium to widen as enterprises consolidate flex as a core commercial real estate category, while competition for MSMEs is likely to intensify their steadier expansion patterns and longer-term value.