The UAE real estate market which was long seen as a global safe haven is now facing one of its sharpest slowdowns in recent years. A report by Goldman Sachs shows that property transaction values dropped 51% month-on-month (MoM) in the first half of March 2026. The decline comes as rising tensions in the Middle East begin to affect investor sentiment.

The ongoing conflict, now in its third week, has begun to weigh on markets across the region, increasing volatility in both energy prices and financial assets. This uncertainty is now reflecting in real estate activity as well. According to analysts at Goldman Sachs, transaction data for early March shows a clear and measurable slowdown in property deals.

In the first half of March 2026, total transaction values in the UAE real estate market declined 31% year-on-year (YoY) and 51% month-on-month (MoM), indicating both a sharp short-term drop and a significant decline compared to last year’s activity levels. The steep MoM fall suggests that the slowdown is closely linked to the recent escalation in geopolitical tensions rather than a gradual market correction.

Recent Market Disruptions (Indicative MoM Impact on Transaction Value)

| Event | Date | Decline |

| Current Middle East Conflict | March 2026 | -51% |

| Iran–Israel conflict | November 2024 | -32% |

| Dubai floods April 2024 | April 2024 | -19% |

| Regional Tensions | June 2025 | -17% |

Note: Figures are indicative and may vary based on dataset, time period, and methodology.

Compared to previous disruptions, the current decline appears more severe. During the Dubai floods April 2024, transaction activity fell by about 19% MoM, largely due to temporary physical disruptions. Similarly, during the Iran–Israel conflict, the decline was around 32% MoM, driven by short-term uncertainty. In June 2025, amid regional tensions, the market saw a relatively moderate drop of 17% MoM. In contrast, the current 51% MoM decline points to a sharper pullback in buyer activity, suggesting that investors are adopting a more cautious, wait-and-watch approach in response to ongoing uncertainty.

Segment Performance: Secondary Market vs. Off-Plan

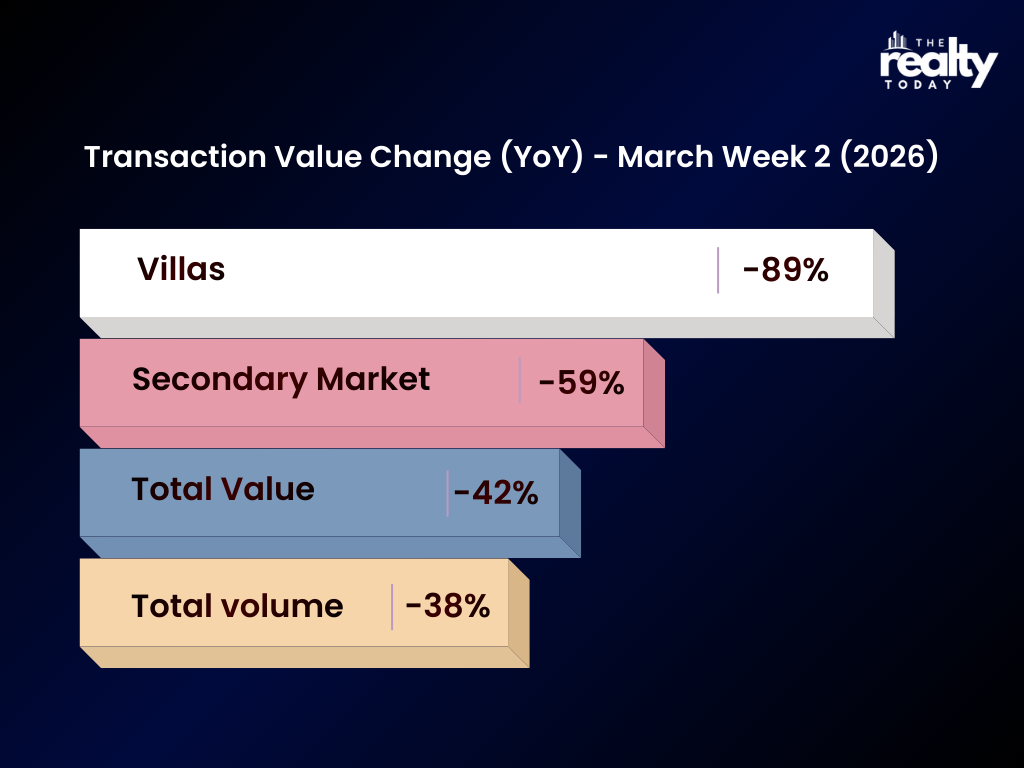

The decline has not been uniform across all sectors. The secondary (ready) market and the luxury villa segment have borne the brunt of the slowdown.

Villas: In the second week of March, villa transaction values collapsed by 89% year-over-year (YoY). This segment, which drove the post-pandemic boom, is highly sensitive to long-term stability concerns.

Secondary Market: Overall transaction values in the secondary market fell by 59% YoY.

- Off-Plan: Transaction volumes in the off-plan segment declined by 38% YoY, with apartment volumes specifically falling by 59%.

Pricing Trends: The First Signs of Softening

For the first time in several years, the "upward only" price trajectory of UAE real estate has hit a plateau.

Apartments: Median prices per square foot dropped 3% YoY and 8% MoM in the first twelve days of March.

Villas: Despite the volume crash, villa prices remained 16% higher than the previous year, though they dipped 2% MoM, indicating that sellers are currently holding their asking prices rather than engaging in panic selling.

Corporate Impact: The Emaar Indicator

The stock market has been a leading indicator of this real estate anxiety. Emaar Properties (DFM: EMAR), the developer of the Burj Khalifa and a bellwether for the sector, saw its shares decline by nearly 40% since the onset of the conflict. This reflects a significant reassessment by institutional investors regarding the projected delivery and sales of the hundreds of thousands of units currently in the pipeline through 2028.

Why This Time is Different

Historically, regional conflict often led to a flight to safety, where capital from unstable neighbors flowed into Dubai and Abu Dhabi. However, several factors make the current situation unique:

Direct Security Concerns: Recent reports of disruptions to regional logistics and a perceived change in the security envelope of the Gulf have unsettled the high-net-worth individuals (HNWIs) who typically view the UAE as a permanent base.

Increased Supply: The market was already facing a wave of supply. With roughly 300,000 to 400,000 units expected to hit the market by 2028, any dip in demand creates an immediate risk of oversupply.

Cost of Finance: With interest rates remaining elevated, the mortgage-backed segment of the market (which accounts for a growing portion of mid-market sales) is less equipped to absorb geopolitical shocks than the cash-heavy market of 2021.

Outlook: Resilience or Realignment?

Despite the staggering 51% MoM drop, many industry experts, including those from Fitch Ratings and Anarock, argue that the fundamentals remain intact. Banks and developers have significantly stronger balance sheets than they did in 2008, with real estate loan exposure sitting at a manageable 14% of total UAE bank loans.

.png)