When you are obtaining a property loan, one of the main decisions that you will face is whether to go for a fixed interest rate or a floating interest rate. You should note that your choice of interest rate kind will have an impact on the amount of money you have to pay monthly. Since loans in real estate are usually for a long time, even a small difference, of a few percent, can affect the amount you pay in total.

Besides that, regarding interest rates in India, the monetary policy of the Reserve Bank of India is very important because it regulates the amount of money you will have to pay back. As a result, you need to understand the two kinds of interest rates before deciding.

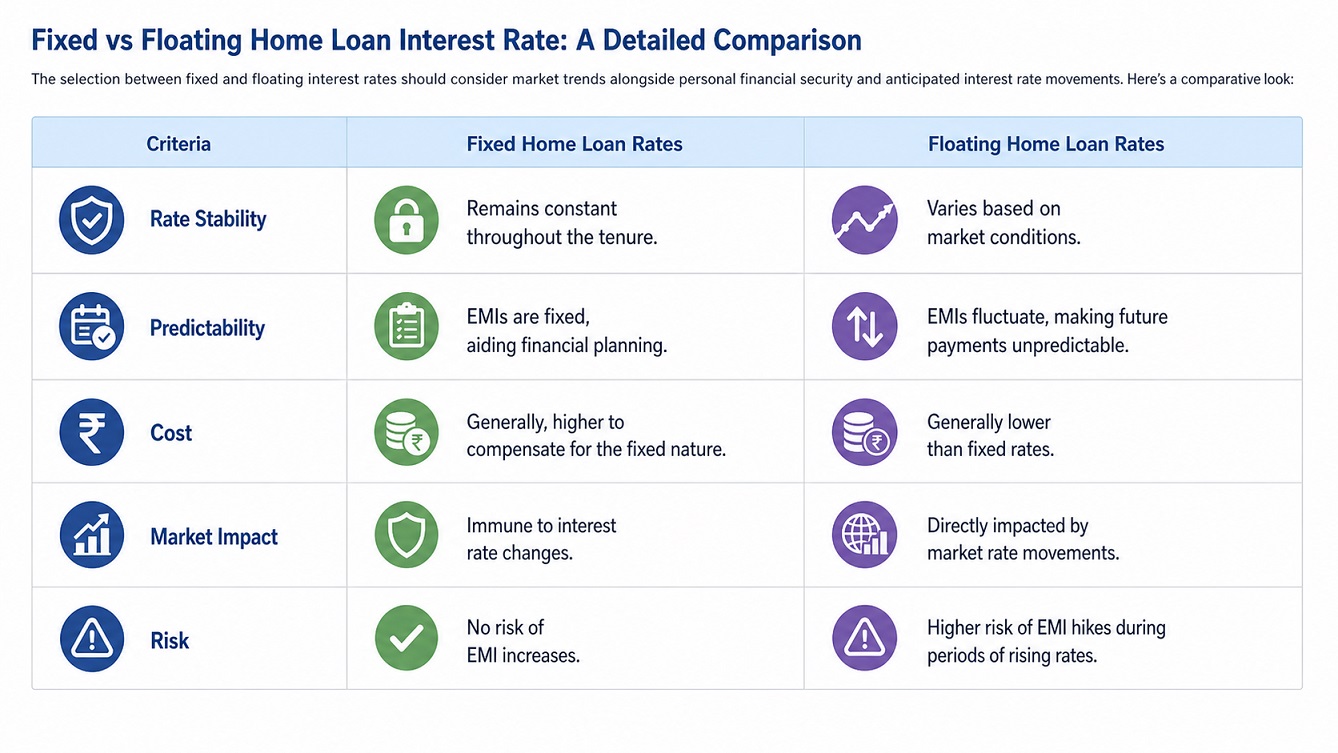

Understanding Fixed Interest Rates

As the term implies, a fixed interest rate will stay unchanged for the specified period of time. It means you can rest assured that your Equated Monthly Installment (EMI) will be the same despite changes in the market environment.

The stability provided by fixed rates may prove invaluable for real estate loan applicants, especially those seeking home loans. After all, such financing entails long-term obligations. The ability to predict how much money you have to pay each month is beneficial when budgeting your finances and making other investment decisions. Moreover, if there are fluctuations in market interest rates due to increased inflation, your EMI will remain the same.

Key Attributes of fixed interest rates:

- Unchanged EMI during the entire loan period

- Protection from interest rate hikes

- Ability to plan finances

- Higher prices compared to floating interest rates

Fixed rates come at a price. Banks take into account possible changes that may affect interest rates in the future, which results in slightly higher prices compared to floating rates. In addition, if market rates decrease, you will not enjoy lower interest payments unless you renegotiate your loan conditions.

Understanding Floating Interest Rates

Floating interest rates, also referred to as variable interest rates, depend on an outside benchmark such as the repo rate of Reserve Bank of India. Since these rates keep changing, your EMI and loan term would also keep varying based on market dynamics.

During the period of falling interest rates, floating interest rate loans can be very beneficial for reducing the burden of your repayments. In case there are increases in interest rates, you could have higher EMIs and even a longer loan term.

Key attributes of floating interest rates:

- Changes according to the state of the market

- Low interest rates than fixed loans at the beginning of the loan term

- EMI/tenure may keep changing from one time period to another

- More influenced by economic cycles

Usually, floating interest rates include a benchmark interest rate and the spread charged by the lender. The combined interest rate keeps changing based on the benchmark rate.

Differences Between Fixed Interest Rate and Floating Interest Rate

The major distinction between fixed and floating interest rate is that while fixed interest rates are not influenced by any economic changes, floating interest rates are influenced by such changes.

- Stability: Fixed interest rate provides stability to the EMI; floating interest rate changes

- Price: Fixed interest rate is expensive; floating interest rate is cheap

- Risk: Fixed interest rate carries little risk; floating interest rate carries more risk

Influence of market: Fixed interest rate is isolated from the market; floating interest rate is influenced by the market

Context of Real Estate: Importance of This Decision

The implications are quite important here because of the lengthy period of repayment and relatively high amount of the loans. Even a slight variation in the rate of interest by one percent is equivalent to thousands of rupees in real estate.

Consider the case of a twenty-year home loan. The loan will react totally differently when it is fixed and floated in the market.

Therefore, it becomes necessary that your decision is well coordinated with not only your capability but also your future interest rate expectations.

Where Fixed Interest Rates Make Sense

Fixed interest rates make more sense in some specific instances. In periods of rising interest rates, or when borrowers value stability over saving money, fixed interest rates are more favorable options.

Cases where fixed interest rates fit better:

- Long-term housing finance for loan periods beyond fifteen years

- Increasing inflation and restrictive monetary policies

- Low-risk borrowers

- Families that earn fixed incomes every month

Here, fixing your interest rate prevents any future increase from affecting your financial plans. This is even more critical for young buyers purchasing their first houses, as they won’t be able to cope with increased EMI payments.

When Are Floating Rates Better?

The following situations may make floating rates more suitable for a borrower:

1. Favorable economic scenario

2. Borrower’s comfort with handling uncertainties

Scenarios in which floating interest rates may prove better:

1. Loan term of 3 to 5 years

2. Declining interest rates

3. Higher income flexibility

4. Prepayment plans

The floating interest rate helps the borrower to save money when the interest rates fall. This may lead to either reduction in EMIs or loan tenure, or both.

Economic Cycles and Their Significance

Interest rates are dynamic in nature and change in cycles based on inflation, economic growth, and monetary policies. In this context, the Reserve Bank of India is instrumental in setting interest rates through changes in the repo rate in order to keep inflation under control and boost economic growth.

- During periods of high inflation, interest rates generally increase

- In times of economic recession, interest rates usually decrease

Knowing the stage of the economy helps borrowers choose either a fixed or floating interest rate.

Effect on Total Interest Rate of the Loan

Whether a borrower opts for a fixed or floating interest rate will determine the total cost of his/her loan. Even though a fixed interest rate is stable and predictable, it could result in an increased amount of total interest rate when interest rates in the market go down. The floating interest rate will increase or decrease depending on how the interest rates vary from time to time.

In a long-term real estate loan, the rate fluctuations might be significant and compound over time.

Important Factors That Need To Be Kept In Mind Before Making Any Decision

There are certain factors which need to be kept in mind before deciding whether one needs to opt for a fixed or floating rate of interest:

- Duration of loan: Fixed rates suit longer duration, whereas floating rates suit shorter duration

- Nature of income: If it is fixed, then fixed rates suit, while if it is unstable, floating rates suit

- Attitude towards risk: Risk-averse individuals prefer fixed rates, whereas risk-prone individuals prefer floating rates

Conclusion

There isn’t one superior type of loan in terms of fixed or floating interest rates for real estate investments. It all comes down to individual preferences and circumstances. The fixed-rate loan ensures certainty and gives you security. The floating rate gives you more leeway, but it comes at a cost – the higher level of risk. The hybrid mortgage is an excellent middle ground, which has the best elements of both types of loans. The idea is not just to pick the lesser evil in terms of a cheaper interest rate but to find the type of financing that will benefit you from a long-term standpoint.